Peer-to-peer (P2P) payments mean digitally transferring money from one individual to another using a Money Transfer Apps. This also means you don’t need to involve traditional financial institutions as an intermediary to do financial transactions. You just need basic details like a phone number, email address, or username to start the payment process.

Mainly, this system was designed for personal use like splitting bills or sending money to family. But now, you can easily make both domestic and cross-border transactions. Not just this, P2P payments are being integrated into banking apps, social platforms, and even cryptocurrency systems to enable users to send money anytime, anywhere with a few taps.

In this blog, we will explore P2P payments apps in depth from the fintech app development company viewpoint, so stay with us

Here are the main types:

You can directly transfer money to other accounts any time or same day using the bank’s apps like cash app or services. It has become easier with P2P payments.

Benefits:

You can send or receive money easily between individuals using Mobile wallet-based P2P payments. They use smartphone apps that store digital money or link to your bank/card.

Benefits:

These payment systems use blockchain technology to transfer money. They are often used for global transfer, especially to help avoid high bank fees.

Benefits:

You can send/ receive money while chatting or interacting using these payment systems.

Benefits:

Third-party P2P payment platforms are considered independent services, since they are not directly operated by banks or messaging apps. They allow users to send, receive, and often store money.

Benefits:

Below are some useful examples of P2P payments in action. These show how we can use them in daily life:

After enjoying dinner with friends, you can pay the bill. Your friends can divide amounts and pay you by using Paytm, Cash App or Google Pay.

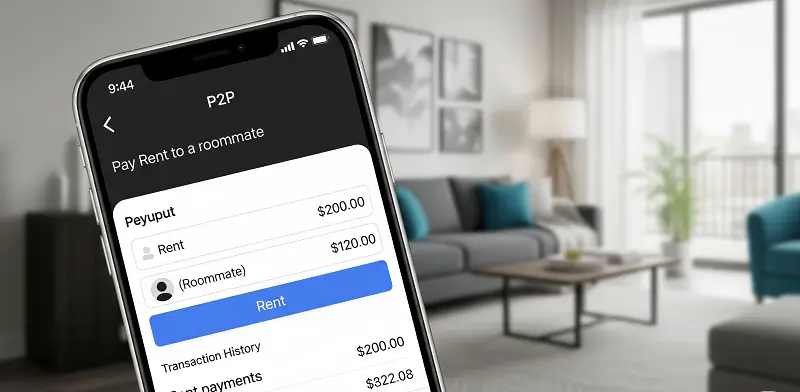

Suppose you are sharing a room, and your share of rent is $ 300. You can easily transfer it to them each month knowing how does zelle work or Paytm.

You buy a second-hand bike from someone through Facebook Marketplace. After checking the bike, you can easily send the money using PayPal or Cash App.

If you live in a different country from your parents. You can send money to them using Wise, Remitly, or crypto Wallets like Bitcoin.

Suppose you hire a graphic designer online. Instead of transferring money through bank accounts, you can pay them using PayPal or UPI for faster and cheaper fintech app development services.

Sometimes, we find ourselves stranded without cash. In such situations, you can receive money from your friends or family through Cash App or Apple Pay.

P2P payments benefit both users and businesses immensely. Let’s take a look:

You just need a smartphone with an internet connection to send money anytime, anywhere. You don’t have to tire yourself out going to the bank or ATM anymore.

P2P payments are great for transferring money in an emergency. Example: Your friends or family need cash urgently, send it in no time through Google Pay or know how does zelle work.

Users don’t have to pay any fees for domestic transfers. Some charge small fees only for credit cards or cross-border transfers.

Anyone can use these payment systems thanks to their user-friendly interfaces. Example: Just scan a QR code to pay a street vendor or taxi driver.

They place high priority on security through encryption, PINs, biometric Login, and fraud monitoring. Example: UPI apps require a PIN before payments.

You can view history or get receipts in the app. The payment history helps you track how much you have spent and where.

They are ideal for situations where physical cash handling is risky or inconvenient. For Example, during COVID-19, where hand-to-hand cash exchange posed a significant health risk.

Choosing the right P2P payment app depends on your needs. This means deciding whether sending money locally, internally, or for personal or business, using Money Transfer Apps. Below are the following tips that can help you decide:

There are multiple aspects relevant to how a transaction occurs in P2P platforms. Let’s take a look:

You need to provide your personal information to verify your identity and link your bank account. Then, set up security features like multi-factor authentication to begin using the services quickly and securely.

If you have to send money to someone, then just enter the recipient’s details and amount to initiate the payment process

This tool checks whether you have enough funds or a linked credit card. It also verifies your identity to help prevent fraud.

You can start sending and receiving money once your account is set up using a phone number or QR code linked to the recipient’s account.

The recipient can keep the money in their app wallet for future use, payments, or transfer it to their bank accounts

All your transactions are encrypted and monitored to prevent fraud and protect data.

Peer to peer payment apps transactions are growing rapidly. It is led by tech innovation, consumer behaviour changes, and regulatory developments. Below are key trends marking the future of P2P payments:

As we can see, P2P payments apps are no longer limited to splitting bills. They are becoming a one-stop shop for financial activities like merging payments, banking, lending, and even making cryptocurrency easy to use on mobile devices. Undeniably, P2P apps represent the future of finance, especially for the next generations.

Vipin Jain is the Co-Founder and CEO at Konstant Infosolutions and is in charge of marketing, project management, administration and R&D at the company. With his marketing background, Vipin Jain has developed and honed the company’s vision, corporate structure & initiatives and its goals, and brought the company into the current era of success.

Or send us an email at: [email protected]